Overfunded 529 Plans: Avoiding Too Much of a Good Thing

The expense of college for children and grandchildren is a troubling issue for almost all of my clients.

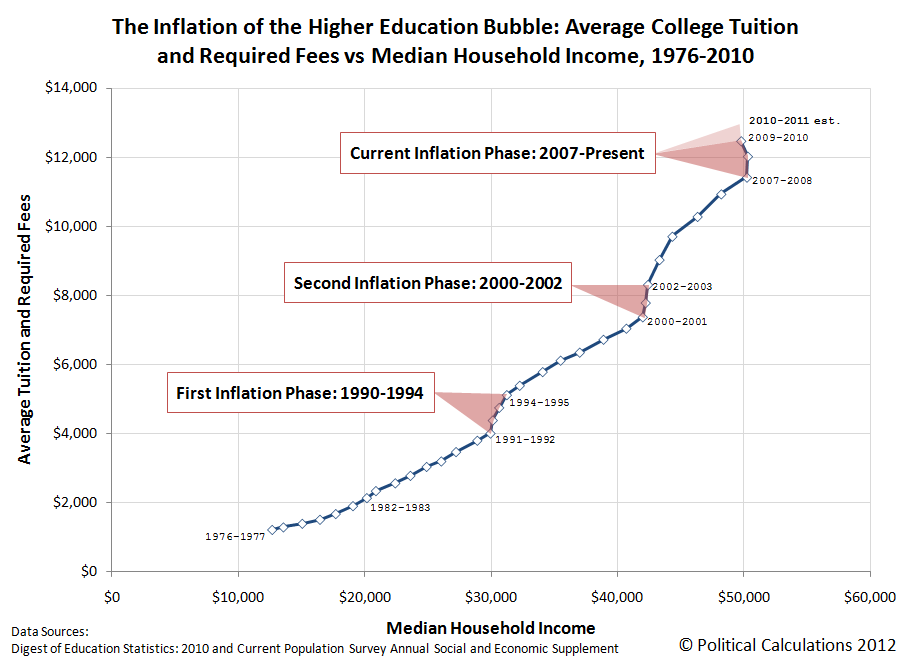

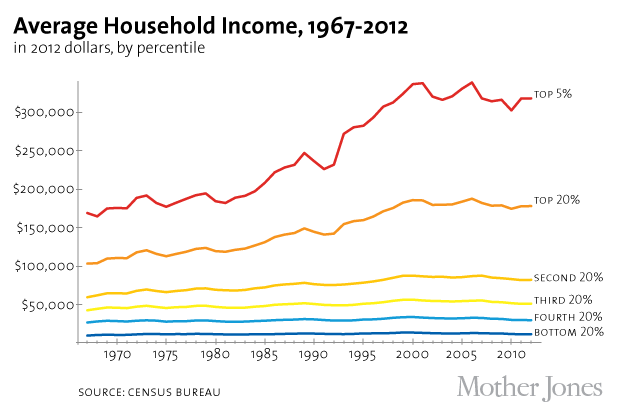

I think this is because at an instinctual level, long before crunching any numbers, clients know what the charts below show: college costs have gone truly exponential in the last one and a half generations, far outstripping increases in the earning power and asset base of the upper middle and lower upper class.

Because the issue is concerning, clients often have a strong instinct to do something, anything, to address the problem. As a result, their attention often turns to Section 529 plans.

Because the issue is concerning, clients often have a strong instinct to do something, anything, to address the problem. As a result, their attention often turns to Section 529 plans.

To evaluate how useful these might be, it’s useful to review their key features.

A 529 plan (sometimes known as a qualified tuition program) has a designated beneficiary and is set up to allow you to either prepay, or contribute to an account established for paying, a student’s qualified education expenses at an eligible educational institution. Total contribution limits to 529 plans vary by state, but generally are at least $300,000 (Kentucky’s is $350,000).

Contributions to 529 plans are not tax deductible for Federal purposes, and (unlike certain other states), Kentucky does not offer state income tax deductions for contributions. Nonetheless, 529 plans do offer a limited income tax benefit, in that account earnings are not taxed until withdrawals occur. In addition, distributions made from 529 plans for qualified educational expenses are not income taxable.

On the down side, distributions from 529 plans that aren’t for qualified educational expenses are income taxable, and incur an additional 10% penalty (which the IRS euphemistically describes as an “additional tax”).

In simple terms, then, you can think of a 529 Plan as somewhat like a Roth IRA for education, with no income limitation on contributions. Our recent post explored whether Roth IRAs really are all they are cracked up to be in many situations.

This post similarly estimates a plausible upper bound on the tax advantages a 529 plan might offer (compared to saving for college in a taxable account), and compares the potential benefits to negative aspects of these plans – notably, their many restrictions, limits, and fees.

Let’s suppose that when a child (Harriet) is born to taxpayers in the highest marginal state + Kentucky income tax bracket of 49.4%, her grandparents are trying to decide whether to contribute $350,000 to Harriet’s 529 plan, or instead put it in a trust or other taxable savings “wrapper”, earmarked for college costs.

I built a model, available here, showing the account’s alternative performance inside and outside the 529 plan. If you like, you can download the worksheet and use your own parameters for tax rates, investment costs, projected inflation rates, and 529 plan costs, to produce a forecast better tailored to your situation.

(If you do that, bear in mind that the model is “back of the envelope” only because it assumes linear investment returns and doesn’t reflect actual period-to-period volatility in those returns.)

In my model run, I used actual costs for Kentucky’s current 529 plan, and low-cost ETF alternatives for bond and broad-based equity exposure. I assumed a 60% stocks, 40% bonds investment mix. For stocks held outside the 529 plan, I assumed long-term holdings until Harriet was 18, and that bond income was taxable each year, used in part to pay taxes, with the remaining bond income reinvested in more bonds. Beyond that, I didn’t model any periodic rebalancing, a simplifying feature that somewhat underestimates actual tax effects of the non-529 plan option.

Note, however, that the model does include the drag caused by 529 plan’s comparatively high fees, relative to low cost index-based passive investments outside 529 plans.

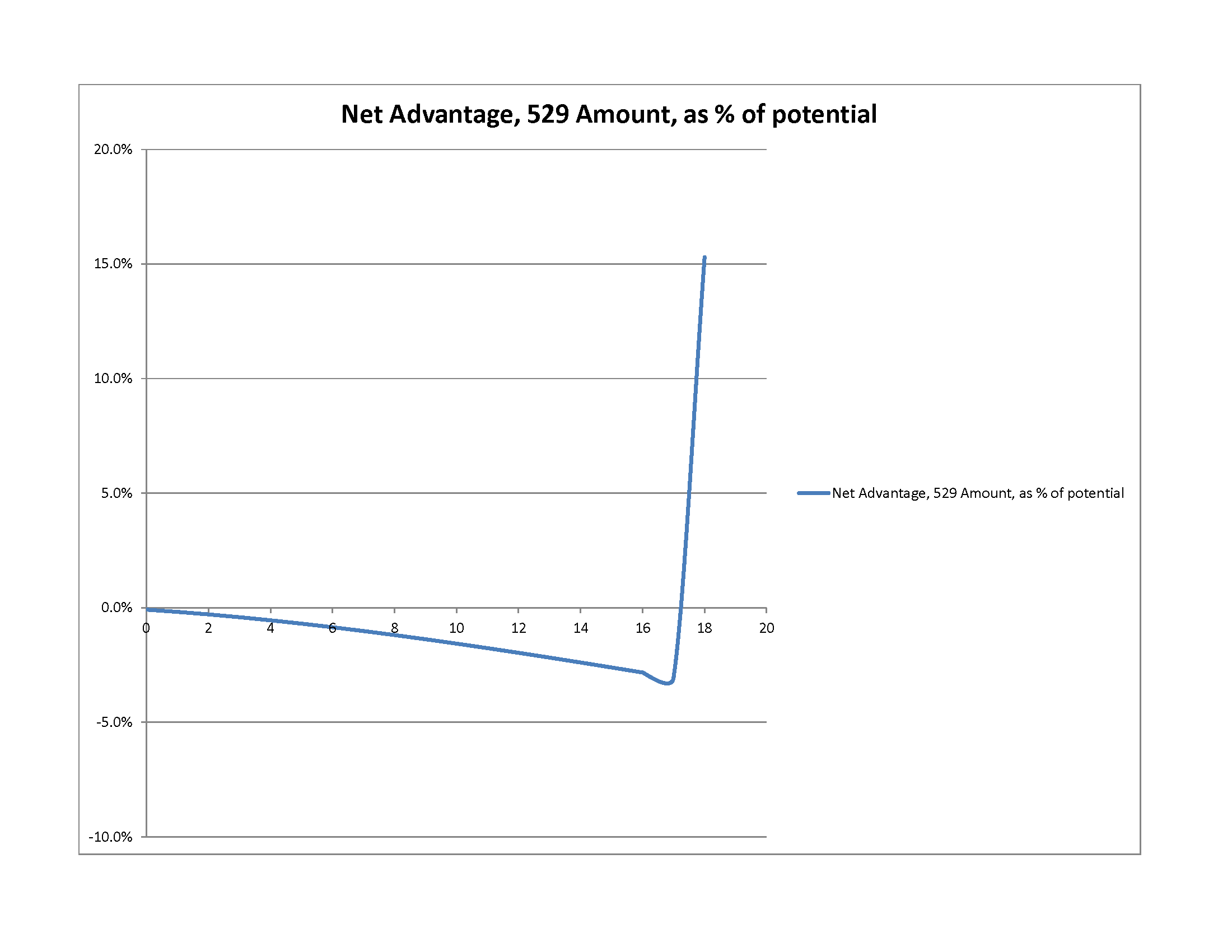

The model suggests that a 529 plan funded with $350,000 for newborn Harriet might reach almost $950,000 by the time she was 18, while a taxable account would reach only $803,000, net of taxes. The net-of-tax advantage for the 529 plan is about 15% of the potential account balance by Harriet’s freshman year. The chart below shows how this advantage accrues in a “pop” at Harriet’s freshman year when withdrawals are taken income tax free, but until then, excess investment costs of the 529 plan cause it to lag taxable alternatives.

So, we’ve learned that a “fully loaded” 529 plan could save as much as $150,000 in taxes. I think if you’re looking for an upper bound on how good these plans can get, that’s a reasonable one.

But, what do you have to give up to get this income tax advantage (again, at its very best, about $150,000, or about 15% of your college funding “kitty”)?

To understand whether the seeming benefits of a 529 Plan will help you — in short, whether the tax advantages these plans offer are worth it — it’s important to understand certain defined terms.

Designated beneficiary. The designated beneficiary is generally the student (or future student) for whom the QTP is intended to provide benefits. The designated beneficiary can be changed after participation in the QTP begins.

Qualified education expenses. These are related to enrollment or attendance at an eligible educational institution.

To be qualified, some of the expenses must be required by the institution, and others must be incurred by students who are enrolled at least half-time.

Expenses that can be qualified if they are required by the institution include tuition and fees and books, supplies, and equipment.

Expenses that can be qualified if incurred by students enrolled at least half-time include room and board (but only room and board not exceeding the cost of attendance used for federal financial aid purposes, or the actual amount charged to the student for housing owned or operating by the institution).

Eligible educational institution. For purposes of a QTP, this is any college, university, vocational school, or other postsecondary educational institution eligible to participate in a student aid program administered by the U.S. Department of Education. It includes virtually all accredited public, nonprofit, and proprietary (privately owned profit-making) postsecondary institutions.

Consider what’s not included in these defined terms, which are the boundary posts on whether funds in the 529 can serve all the purposes a family might want them to.

Qualified education expenses don’t include boarding school tuition, summer camps, travel team expenses, or trips to Europe. They don’t include stipends to cover living expenses during an unpaid internship. They don’t include brokers’ fees and a deposit on an apartment in the big city for a first job after graduation. They don’t include the cost of a car to get a student to and from college and graduate school. They don’t include wedding expenses, or a down payment on a home.

In short, qualified education expenses don’t include a great many of the ways families actually spend money to launch their children and grandchildren in life.

Another pitfall of 529 plans is that they generally offer limited investment choices, which can only be changed selections once per year. If a family has a great investment idea, or a particular risk aversion, or a single-stock or single-industry concentration to manage, they have a really difficult time doing that with 529 plan assets.

Those are the main reason I usually encourage families to be very thoughtful when evaluating 529s – to consider the flexibility they are surrendering in order to obtain a relatively limited-scale income tax benefit.

If a 529 plan is funded at a level targeted to cover actual qualified education expenses a student will have in the future, while avoiding overfunding, it’s possible to capture the income tax advantages, while avoiding the pitfalls outlined above.

To explore this issue, I modeled current qualified education expenses for undergraduates at Vanderbilt, as a proxy for private college costs. (These seem to be about $239,000.)

If these expenses continue to grow at twice the general projected inflation rate (see here for more on how to determine projected inflation rates), 18 years from now they will be approximately $420,000. In the example discussed above, Harriet’s “maxed out” 529 plan would be overfunded to the tune of over $525,000!

You can “goal seek” the model to explore target funding amounts (in our example, the model suggests a 529 funded with about $155,000 would fully fund qualified education expenses, while avoiding overfunding).

I think the case for 529 plans is much like the case for Roth IRAs: conceptually, they’re attractive, but it’s critical not to deal in generalities. Instead, evaluate your specific facts very carefully, particularly your likely time horizons, your current and future asset base, and your income growth trajectory.

Only then will you be able to make decisions about 529 plans for your family that appropriately balance flexibility and tax savings opportunities, and avoids the frustration of a substantially overfunded 529. (In a future post, we’ll discuss options for what to do if you do end up with an overfunded 529 plan.)